Pandemic or Not, You Can’t Predict Bubbles, So Stop Trying

Will the pandemic continue to rage and cripple the global market? Will, we hit a tech bust? Will Tesla shares and stocks, in general, come spiraling down? It’s certainly possible,

When Financial Knowledge Counts

The global economy grows increasingly complex. Like reading or writing, economic literacy is an essential life skill. Whether young, old, or older, wealthy or barely making it, married or not

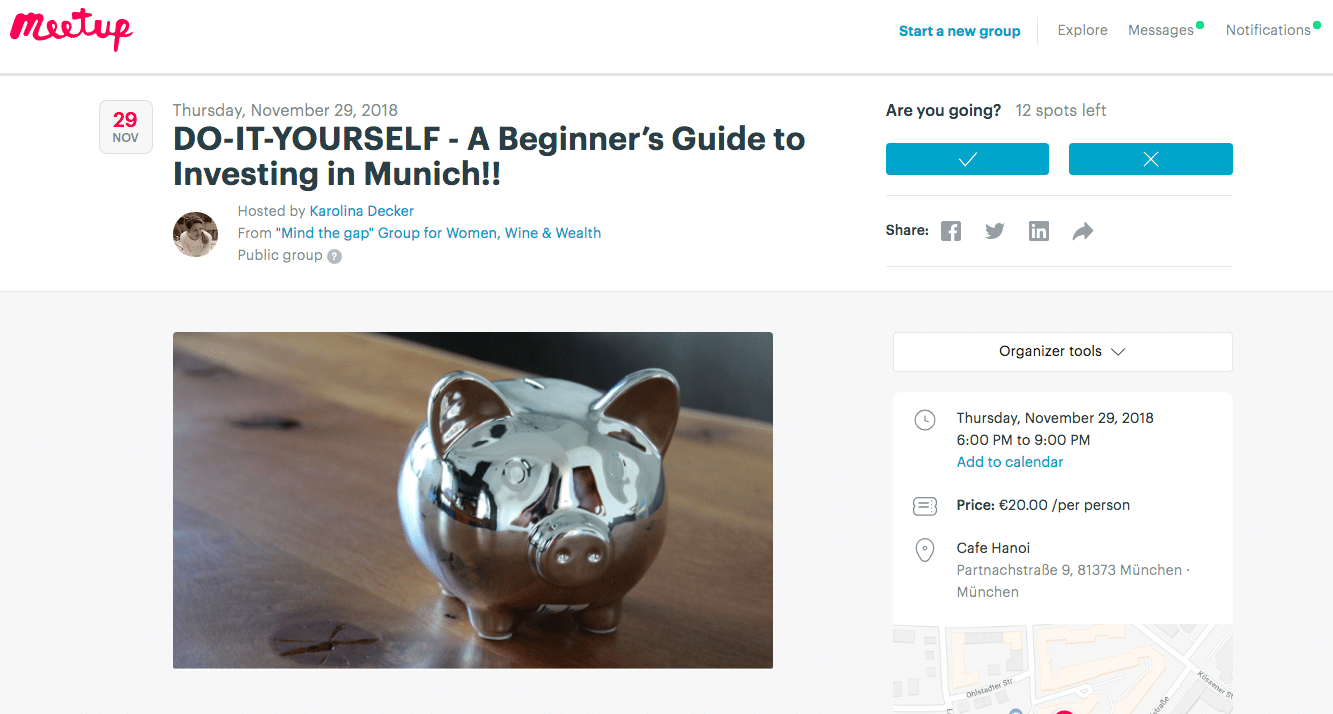

Meet Finanzdiva in Munich (29/11/18)

Find out all about our collaboration with Finanzdiva and get ready for our upcoming event in Munich: A Beginner’s Guide to Investing, on 29th November. See you there!

Discover the World of Ethical Investing

We all want our investments to be sustainable and protect human rights, but it’s not always easy to tick every ethical and environmental box. Finanzdiva shares her top six things

Investment Income Tax in Germany: A Fairytale by Finanzdiva

Our friend and favourite finance maven, Finanzdiva, comes with hot tips and tricks to help you save money, time and nerves on investment income taxes. Once upon a time,

Saving Money: Goals For Each Stage of Life

Thinking about the distant future is not always easy or appealing, but it is really important. Whether it’s buying a house or living comfortably once you stop working, forward